Ratings assigned on long-term and short-term rating scales of VIS Rating are forward-looking opinions of the relative credit risks of an entity, debt or financial obligation, debt security, preferred share or other financial instruments, or of an issuer of such a debt or financial obligation, debt security, preferred share or other financial instruments in Vietnam.

A rating of VIS Rating addresses the issuer’s ability to obtain cash sufficient to service the debt obligation, and its willingness to pay[1]. VIS Rating defines credit risk as the risk that an entity/issuer may not meet its contractual financial obligations as they come due and any estimated financial loss in the event of default or impairment. Especially at the lower end of the rating scale, typically CCC and below, ratings typically include additional considerations that reflect our expectations for recovery of principal and interest, as well as the uncertainty around that expectation.

Long-term ratings are assigned to issuers or debt instruments with an original maturity of one year or more and reflect both the likelihood of a default or impairment on contractual financial obligations and the expected financial loss suffered in the event of default or impairment.

Short-term ratings are assigned to debt instruments with an original maturity of 13 months or less and reflect both the likelihood of a default or impairment on contractual financial obligations and the expected financial loss suffered in the event of default or impairment.

VIS Rating issues ratings at the issuer level and debt instrument level on both the long-term scale and the short-term scale. Typically, ratings are made publicly available, although private and unpublished ratings may also be assigned.

VIS Rating long-term ratings are opinions of the relative creditworthiness of issuers or debt instruments with an original maturity of one year or more within Vietnam.

|

Long-Term Rating Scale |

|

|

AAA |

Issuers or debt instruments rated AAA demonstrate the strongest creditworthiness relative to other domestic entities and transactions. |

|

AA |

Issuers or debt instruments rated AA demonstrate very strong creditworthiness relative to other domestic entities and transactions. |

|

A |

Issuers or debt instruments rated A demonstrate above-average creditworthiness relative to other domestic entities and transactions. |

|

BBB |

Issuers or debt instruments rated BBB demonstrate average creditworthiness relative to other domestic entities and transactions. |

|

BB |

Issuers or debt instruments rated BB demonstrate below-average creditworthiness relative to other domestic entities and transactions. |

|

B |

Issuers or debt instruments rated B demonstrate weak creditworthiness relative to other domestic entities and transactions and may be approaching default, with strong recovery prospects. |

|

CCC |

Issuers or debt instruments rated CCC demonstrate very weak creditworthiness relative to other domestic entities and transactions and are likely in or near default, typically with moderate recovery prospects. |

|

CC |

Issuers or debt instruments rated CC demonstrate extremely weak creditworthiness relative to other domestic entities and transactions and are typically in default, typically with poor recovery prospects. |

|

C |

Issuers or debt instruments rated C demonstrate the weakest creditworthiness relative to other domestic entities and transactions and are typically in default, with very poor recovery prospects. |

|

Note: VIS Rating appends the modifiers + and - to each generic rating classification from AA through CCC. The modifier + indicates that the obligation ranks in the higher end of its generic rating category; no modifier indicates a mid-range ranking; and the modifier - indicates a ranking in the lower end of that generic rating category. |

|

Short-term ratings of VIS Rating are opinions of the ability of issuers in Vietnam, relative to other domestic issuers, to repay their debt obligations that have an original maturity not exceeding 13 months.

There are five categories of short-term national scale ratings, as defined below.

|

Short-Term Rating Scale |

|

|

A-1 |

Issuers rated A-1 have the strongest ability to repay short-term senior unsecured debt obligations relative to other domestic entities and transactions. |

|

A-2 |

Issuers rated A-2 have an above-average ability to repay short-term senior unsecured debt obligations relative to other domestic entities and transactions. |

|

B-1 |

Issuers rated B-1 have an average ability to repay short-term senior unsecured debt obligations relative to other domestic entities and transactions. |

|

B-2 |

Issuers rated B-2 have a weak ability to repay short-term senior unsecured debt obligations relative to other domestic entities and transactions. |

|

C-1 |

Issuers rated C-1 have the weakest ability to repay short-term senior unsecured debt obligations relative to other domestic entities and transactions. |

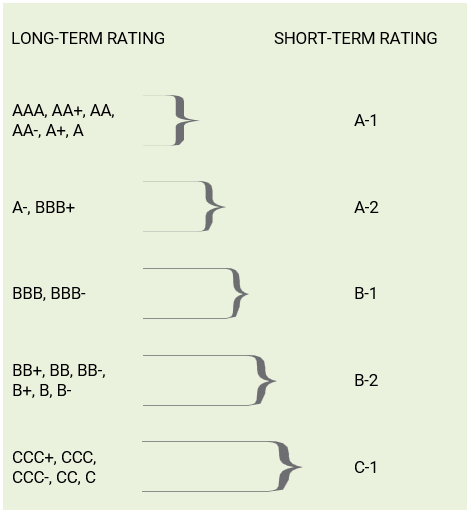

The following table indicates the long-term ratings consistent with different short-term ratings when such long-term ratings exist.

Short-term ratings are based on this mapping in cases where the issuer has liquidity that is commensurate with its long-term rating category, or stronger. In assigning short-term ratings, we typically also consider the sources and uses of an issuer’s liquidity over the next 12-15 months. As a result, in some cases, short-term ratings may be assigned at a level that is lower than indicated by the standard linkage.

Issuer Ratings

Issuer Ratings are opinions of the ability of entities to honor senior unsecured debts and other debt instruments. Issuer Ratings incorporate any meaningful external support that is expected to benefit unsecured creditors generally but do not incorporate support arrangements (e.g., guarantees) that apply only to specific senior unsecured financial obligations.

Medium-Term Note Program Ratings and Debt Instrument Ratings

VIS Rating assigns debt instrument ratings to medium-term note (MTN) programs and to the individual debt securities issued from them (referred to as drawdowns or notes). MTN program ratings are intended to reflect the ratings likely to be assigned to drawdowns issued from the program with the specified priority of claim (e.g., senior or subordinated).

Provisional Ratings

VIS Rating may assign a provisional rating to an issuer or a debt instrument when the change to a definitive rating is subject to the fulfillment of contingencies that could affect the rating. Examples of such contingencies are the finalization of transaction documents/terms where a rating is sensitive to changes at closing. When such contingencies are not present, a definitive rating may be assigned based on documentation that is not yet in final form. A provisional rating is denoted by placing a (P) in front of the rating. The (P) notation provides additional information about the rating but does not indicate a different rating. For example, a provisional rating of (P)AA+ is the same rating as AA+.

For provisional ratings assigned to an issuer or debt instrument, the (P) notation is removed when the applicable contingencies have been fulfilled.

When VIS Rating no longer rates an issuer or debt instrument on which it previously maintained a rating, the symbol WR is employed.

NR is assigned to an unrated issuer, debt instrument and/or program.

VIS Rating’s definition of default is applicable only to debt instruments. The following events constitute a debt default under our definition:

1. A missed or delayed disbursement of a contractually obligated interest or principal payment (excluding missed payments cured within a contractually allowed grace period), as defined in credit agreements and indentures;

2. A bankruptcy filing or legal receivership by the debt issuer or obligor that will likely cause a nonpayment or delay in future contractually obligated debt service payments;

3. A distressed exchange whereby (i) an issuer offers creditors a new or restructured debt, or a new package of securities, cash or assets that amount to a diminished value relative to the debt obligation’s original promise; and (ii) the exchange has the effect of allowing the issuer to avoid a likely eventual default;

4. A change in the payment terms of a credit agreement or indenture that results in a diminished financial obligation.

Our definition of default does not include so-called “technical defaults,” such as maximum leverage or minimum debt coverage violations unless the obligor fails to cure the violation and fails to honor the resulting debt acceleration that may be required.

Also excluded are payments owed on long-term debt obligations that are missed due to purely technical or administrative errors that are (i) not related to the ability or willingness to make the payments; and (ii) are cured in very short order (typically, 1-2 business days after the error is recognized). Finally, in select instances based on the facts and circumstances, missed payments on financial contracts or claims may be excluded if they are the result of legal disputes regarding the validity of those claims.

A security is impaired when investors receive — or expect to receive with near certainty — less value than would be expected if the obligors were not experiencing financial distress or otherwise prevented from making payments by a third party, even if the indenture or contractual agreement does not provide the investor with a natural remedy for such events, such as the right to press for bankruptcy.

VIS Rating’s definition of impairment is applicable to debt instruments. A debt instrument is deemed to be impaired upon any of the following:

1. Any of the events that meet our definition of default have occurred;

2. Contractually allowable payment omissions of scheduled interest or principal payments on debt instruments;

3. Downgrades to CC or C, signaling the near certain expectation of a significant level of future losses;

4. Write-downs or impairment distressed exchanges[2] on debt instruments due to financial distress whereby (i) the principal promise to an investor is reduced according to the terms of the indenture or other governing agreement[3]; or (ii) an obligor offers investors a new or restructured debt, or a new package of securities, cash or assets, and the exchange has the effect of allowing the obligor to avoid a contractually allowable payment omission as described in (2) above.

Credit Rating Methodologies describe the analytical framework that VIS Rating’s Credit Rating councils use to assign credit ratings. They set out the key analytical factors which VIS Rating believes are the most important determinants of credit risk for the relevant sector. Credit Rating Methodologies are not exhaustive treatments of all factors reflected in ratings of VIS Rating; they simply set out the key qualitative and quantitative considerations used by VIS Rating in determining ratings. In order to help third parties to understand VIS Rating’s analytical approach, all Credit Rating Methodologies are publicly available.

A rating outlook of VIS Rating is an opinion regarding the likely rating direction over the medium term. Rating outlooks fall into four categories: Positive (POS), Negative (NEG), Stable (STA), and Developing (DEV). Outlooks may be assigned at the issuer level or at the debt instrument level.

A designation of RUR (Rating(s) Under Review) indicates that an issuer has one or more ratings under review, which overrides the outlook designation. A designation of RWR (Rating(s) Withdrawn) indicates that an issuer has no active credit ratings to which an outlook is applicable.

A stable outlook indicates a low likelihood of a rating change over the medium term. A negative, positive or developing outlook indicates a higher likelihood of a rating change over the medium term. A Credit Rating council that assigns an outlook of stable, negative, positive, or developing to an issuer’s rating is also indicating its belief that the issuer’s credit profile is consistent with the relevant rating level at that point in time.

A review indicates that a rating is under consideration for a change in the near term. A rating can be placed on review for upgrade (UPG) or downgrade (DNG). A review may end with a rating being upgraded, downgraded, or confirmed without a change to the rating. Ratings on review are said to be on VIS Rating’s “Watchlist” or “On Watch”. Ratings are placed on review when a rating action may be warranted in the near term, but further information or analysis is needed to reach a decision on the need for a rating change or the magnitude of the potential change.

A Confirmation is a public statement that a previously announced review of a rating has been completed without a change to the rating.

An Affirmation is a public statement that the current Credit Rating assigned to an issuer or debt instrument, which is not currently under review, continues to be appropriately positioned. An Affirmation is generally issued to communicate VIS Rating’s opinion that a publicly visible credit development does not have a direct impact on an outstanding rating.

VIS Rating means Vietnam Investors Service And Credit Rating Agency Joint Stock Company, a company incorporated under the laws of Vietnam with enterprise code 0109839192 issued by the Department of Planning and Investment of Hanoi on 30 November 2021 and head office at Unit 2709, 27th floor – West Tower, Lotte Center Hanoi Building, 54 Lieu Giai, Cong Vi Ward, Ba Dinh District, Hanoi City, Vietnam.

[1] In some cases, credit risk may relate to a party other than the issuer, e.g., a guarantor. For issuer-level ratings, please see the definition of Issuer Ratings in this document.

[2] Impairment distressed exchanges are similar to default distressed exchanges except that they have the effect of avoiding an impairment event, rather than a default event

[3] Failures to pay principal as contractually required are defaults. Once written down, complete cures, in which securities are written back up to their original balances, are extraordinarily rare; moreover, in most cases, a write-down of principal leads to an immediate and permanent loss of interest for investors, since the balance against which interest is calculated has been reduced.

Tiếng Việt

Tiếng Việt

English

English