In this credit rating methodology[1], we explain our general approach to assessing credit risk for non-financial corporates in Vietnam and to assigning issuer ratings and debt instrument-level ratings[2]. Our definition of non-financial corporates encompasses a broad range of non-financial industry sectors including construction, manufacturing, metals and mining, real estate developers, regulated utilities, and transportation among others.

We discuss the qualitative and quantitative factors that are likely to affect rating outcomes in these sectors. We also discuss other considerations, which are factors for which the credit importance may vary widely among the companies in these sectors or may be important only under certain circumstances or for a subset of companies. We also discuss our approach to assessing the potential for affiliate support and the potential for government support. Since credit ratings are forward-looking, we often incorporate directional views of risks and mitigants in a qualitative way.

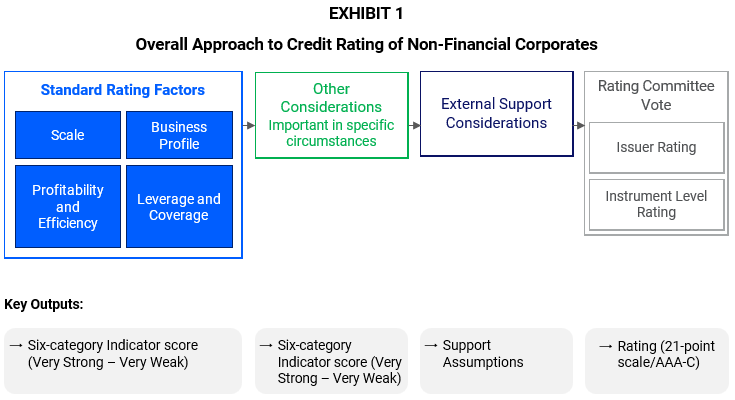

Our presentation of this credit rating methodology proceeds with (i) a discussion of the standard rating factors; (ii) other considerations; (iii) assessing support; (iv) assigning issuer and debt instrument-level ratings; and (v) general limitations.

Source: VIS Rating

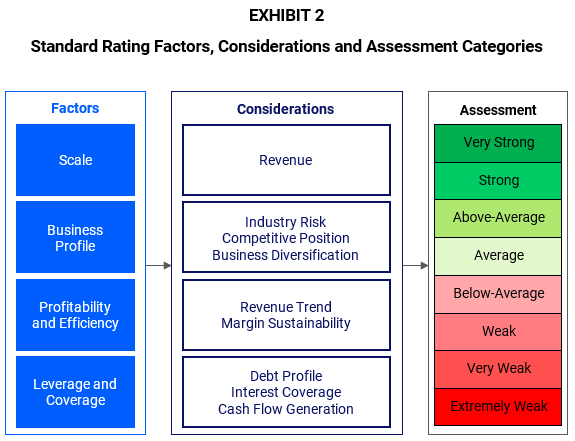

In this section, we explain our general approach for assessing each standard rating factor, and we describe why it is meaningful as an indicator of credit quality for companies rated under this methodology. We typically characterize each issuer rated under this methodology as a non-financial corporate operating in a specific industry sector. The designation of an issuer into one of these industry sectors informs our assessment of each of the standard rating factors. We consider the standard rating factors, which include the assessment of the company’s scale, its business profile, profitability, efficiency, and its leverage and coverage. For each factor, we will assess based on an eight-category scale: Very Strong, Strong, Above-Average, Average, Below-Average, Weak, Very Weak, and Extremely Weak. In the following sections, we assess other considerations and incorporate the potential for support from a parent company, affiliate, or other entity to arrive at the credit rating.

Source: VIS Rating

Our assements are forward-looking and reflect our expectations for future financial and operating performance. However, historical results are helpful in understanding patterns and trends of a company’s performance as well as for peer comparisons. Historical financial ratios for non-financial corporates, unless otherwise indicated, are typically calculated based on an annual or 12-month period. Nonetheless, financial ratios can be assessed using various time periods. For example, credit rating councils may find it analytically useful to examine both historical and expected future performance for periods of several years or more which may be impacted by factors such as expected changes in macroeconomic conditions, market dynamics, business environment, as well as company-specific factors such as corporate strategy and governance, key personnel risks etc.

In the financial metrics we use, we consider how well financial reporting mirrors economic reality. Where the economics of an issuer or transaction are not fully reflected in financial reporting, we may make analytic adjustments to financial statements to facilitate our analysis.

Scale reflects the overall depth of a company’s business and its success in attracting a variety of customers, as well as its resilience to shocks, such as sudden shifts in demand or rapid cost increases. A larger company is also typically in a stronger position to negotiate with distributors, suppliers, and service providers for better terms, including lower costs. Scale also tends to closely track other positive characteristics, such as operating efficiency, longevity, and access to capital markets.

How We Assess It

We based our initial assessment using a company’s reported revenues.

The business profile of a company is important because it reflects a company’s business strategy and greatly influences its ability to generate sustainable earnings and operating cash flow. Core aspects of a company’s business profile are its industry profile and its competitive position and business diversification. These aspects of the business profile typically have a considerable impact on the stability and sustainability of a company’s revenue and profit margins over the long term.

A key component of our analysis is the extent to which industry-specific environment and conditions can have a meaningful influence on the credit profiles of a company. We view companies operating in industry sectors with weaker industry profiles (i.e., higher industry risks) to be more exposed to industry-specific pressures that may create vulnerabilities to their business model and operating performance.

How We Assess It

We assess an industry’s barriers to entry, extent of competition, volatility in business performance, and growth outlook. We generally consider industries with a stronger industry profile to have more favorable operating conditions for companies within that industry relative to others, which in turn, will be credit positive for the future financial performance and viability of the company.

High barriers of entry, for example, licensing requirements and ownership of key technical capabilities, can serve as an advantage against potential new entrants and allow companies to defend their market positions. Companies operating in highly fragmented industries with little product or service differentiation are more likely to face intense competitive pressures.

Industries that are more sensitive to business cycles – for example real estate, manufacturing, metals and mining - typically experience higher volatility and larger swings in their business performance.

Companies operating in industries with stronger growth prospects – for example, rising demand for products and services, new business opportunities driven by the adoption of new technology – are more likely to benefit from improving operating environment and business revenue.

A company’s competitive position is also typically a meaningful indicator of its corporate strategy, brand, and reputational strength, access to capital, cost structure, and resilience to economic downturns and to intensifying competition.

How We Assess It

We assess a company’s market position, operational efficiency, and competitive advantage in its key industry and/or product sectors. We also consider a company’s track record in corporate execution.

We assess market position across a company’s business segments, typically where a segment comprises a suite of products and services generally oriented to serving a set of customers. Core segments are those that represent key competencies of the company and a material portion of the company’s revenue and cash flow.

Companies with leading competitive positions generally benefit from economies of scale, advantageous cost structure, or have more of an ability to pass on cost increases to customers and may have stronger negotiating power with suppliers and other related parties. Typically, a company with a strong competitive position and high relevance to customers, based on its brands or the types of products or services that it offers, has high customer loyalty, generally leading to more recurring sales, stronger profit margins and higher operating flexibility through the cycle than a company with a weaker competitive position and less relevance to customers.

Companies with multiple business segments and a wide range of product offerings tend to generate more stable revenue and profit margins compared with competitors that have a narrower business focus. Conversely, companies that rely on one product or a small number of products may be more vulnerable to economic shocks, competitive pressures, or shifts in demand and experience greater volatility. Geographic diversity is an important aspect of business diversity because it reduces a company’s exposure to adverse regional, customer, or vendor-specific developments that could cause shifts in product demand, fluctuations in price, or supply disruptions.

How We Assess It

We consider the diversity of core products and the extent or concentration of a company’s customer base in different segments. We also consider its geographic footprint of sales, physical outlets, and plants.

In assessing the diversity of the company’s core products, we consider the number and mix of segments and their contribution to sales and profitability. In general, we consider core product segments to be those that represent key competencies of the company and a material portion of the company’s revenue and cash flow.

We consider the diversity and range of the company’s customer base in its main sectors and the potential for revenue to decrease due to changes in preferences among its top customers or largest targeted consumer segment.

Our assessment of geographic diversification is primarily based on the diversity of a company’s end markets within Vietnam, and whether it also has a meaningful presence in markets outside of the country.

The strength of a company’s profitability is typically a function of its revenue trajectory and the sustainability of its profit margins, considering the expected changes in macroeconomic conditions, market dynamics, and business environment. A company with strong profitability and operating efficiency can generally withstand economic and cyclical downturns, and faces less strategic risks with less impact on its credit metrics and its ability to pay debt and other obligations than a company with weaker profitability and operating efficiency.

How We Assess It

In assessing profitability and efficiency for non-financial corporates, we qualitatively assess revenue trends and profit margin sustainability. In our assessment, we consider the level, trajectory, and sustainability of profit margins and revenue.

We typically consider, among other things, the extent of a company’s operational flexibility and its capacity and willingness to take the steps necessary to maintain or support profit margin levels. We also typically assess the drivers behind revenue growth (e.g., market dynamics, organic growth, or mergers and acquisitions) and the risks associated with those drivers.

Leverage and cash flow coverage measures provide important indications of a company’s financial flexibility and long-term viability. Strength in this area is an indicator of a company’s investment capabilities and its ability to withstand fluctuations in the business cycle, respond to unexpected challenges, and pay debt.

We consider a range of quantitative ratios that measure a company’s leverage profile, interest coverage, and cash flow generation. A low ratio of debt to EBITDA, robust interest expense coverage, and strong cash flow to debt ratio typically indicate a strong ability to adapt to changes in their respective markets and competitive environment.

The ratio of the company’s total debt to earnings before interest, taxes, depreciation, and amortization (EBITDA) is an indicator of debt serviceability and leverage. The ratio is commonly used as a proxy for comparative financial strength.

The ratio of earnings before interest and taxes (EBIT) to financial expenses is an important indicator of a company's ability to pay its interest obligations and other financial expenses from its earnings, measured or estimated by EBIT, after giving consideration for the depreciation of its assets, a measure of minimum capital expenses to maintain normal business operations.

The ratio of cash flow from operations (CFO) or funds from operations (FFO) to debt is an indicator of a company’s financial flexibility. For non-financial corporates, CFO to debt provides an indication of the company’s cash generation after internal working capital needs but before dividends and capital expenditures relative to its debt burden.

The ratio of retained cash flow (RCF) to debt provides insight into the company’s cash flow generation, before working capital movements (i.e. FFO) and after dividend payments, in relation to debt. The higher the level of retained cash flow relative to a company’s debt, the more cash the company has to finance its working capital, capital expenditures, acquisitions and/or any debt reduction.

How We Assess It

Debt / EBITDA:

The numerator is total debt, and the denominator is EBITDA.

EBIT / Financial Expenses:

The numerator is EBIT, and the denominator is financial expenses. For this calculation or estimation, we adjust financial expenses to remove the effects of foreign currency exchange rates.

CFO / Debt:

The numerator is cash flow from operations (CFO), and the denominator is total debt.

FFO / Debt:

The numerator is funds from operations (FFO), and the denominator is total debt.

RCF / Debt:

The numerator is FFO minus dividends (retained cash flow (RCF)), and the denominator is total debt.

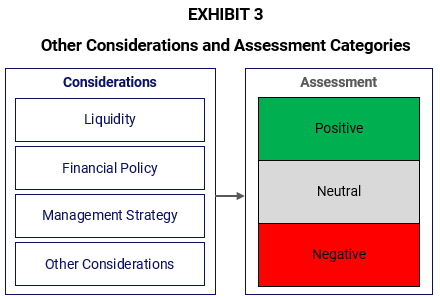

In assigning a credit rating, we may assess additional considerations that are not incorporated into the standard rating factors. Some of these considerations may be important to all companies in this sector, while others may be important only under certain circumstances or for a subset of companies. Each consideration is assessed based on a three-category scale: Positive, Neutral, Negative. For companies with Positive assessments, we may incorporate positive adjustments to arrive at their credit ratings. Conversely, credit ratings of companies with Negative assessments may incorporate negative adjustments.

Source: VIS Rating

Below are examples of other considerations that may be reflected in our ratings.

Liquidity is a particularly important consideration for companies that have less operating and financial flexibility, and ratings can be heavily affected by extremely weak liquidity. We form an opinion on a company’s likely near-term liquidity requirements from the perspective of both sources and uses of cash. We may also consider how stress scenarios can affect a company’s liquidity. In such cases, we could consider seasonality in our analysis.

Financial policy encompasses the company’s tolerance for financial risk and commitment to a strong credit profile. It directly affects risk appetite, capital allocation, debt levels, credit quality, the future direction for the company, the strategic risks faced by the company, and the risk of adverse changes in financing and capital structure. Considerations typically include the issuer’s desired capital structure or targeted credit profile, its ability to adhere to its commitments even when faced with challenges, and its track record of risk and liquidity management.

The quality of management is an important factor supporting a company’s credit strength. Assessing the execution of business plans over time can be helpful in assessing management’s business strategies, policies, and philosophies and in evaluating management performance relative to the performance of competitors and our projections. Management's track record of adhering to stated plans, commitments, and guidelines provides insight into management’s likely future performance, including in stressed situations.

A demonstrable financial track record can be instrumental in allowing a non-financial corporate to access credit and raise capital, which are generally necessary for growth, and which support its ability to withstand a down cycle. For companies that lack financial history, our projections may reflect more conservative expectations than management’s projections.

We rely on the accuracy of audited financial statements to assign and monitor ratings for companies rated under this methodology. The existence of relevant and timely financial information, disclosure, and the consistent application of financial information can indicate a company’s corporate governance and transparency as well as its compliance with its policies and regulatory standards. Auditors’ reports and comments, unusual restatements of financial statements, or delays in regulatory filings may indicate weaknesses in internal controls.

Environmental, social and governance (ESG) considerations may affect the ratings of issuers in different sectors differently. In many sectors, all issuers have a similar level of exposure to ESG risks. In these cases, ESG risks may differentiate ratings in the sector relative to other sectors, but they typically only differentiate ratings within the same sector when an issuer is unusually strong or weak in a particular aspect of ESG. In other sectors, some ESG issues can vary widely across issuers and be important only under certain circumstances or for a subset of issuers within that sector.

For example, our assessment of governance considers a corporate’s ownership and control, board oversight and effectiveness, and management structure and compensation.

ESG issues typically have disproportionate downside risks. However, ESG considerations are not always negative, and they can be a source of credit strength in rare instances. For example, a company that has outstandingly strong governance is more likely to have a management culture of full-degree risk assessment and informed decision-making with a view toward long-term sustainability.

We recognize the possibility that an unexpected event could cause a sudden and sharp decline in a company’s fundamental creditworthiness. Event risks — which are varied and tend to have low probability and high impact — can overwhelm even a stable, well-capitalized company. Some types of event risks include mergers and acquisitions, asset sales, spin-offs, litigation, pandemics, significant cyber-crime events, and shareholder distributions.

In addition to the rating factors and other considerations, ratings of non-financial corporates in Vietnam incorporate our assessment of support – explicit or implicit – from a parent company, affiliate, government, or other entity.

Explicit support is generally provided in the form of capital injections to the supported company. Less frequently, a parent or affiliate may provide a direct guarantee that is usually intended to transfer the credit risk of the support provider to the supported company. In assessing explicit support, we consider the specific legal nature and enforceability of the support as well as the likelihood of timely payment and its possible termination.

For implicit, non-legally binding support, we consider the support provider’s capacity to provide support, and its willingness to support. Our assessment of the benefit to a company’s credit profile is primarily based on our assessment of the financial strength of the support provider, the extent of the strategic linkage and integration of business operations between the company and its support provider, and/or past evidence of support. Conversely, we also consider the potential credit drag on the company’s credit profile that may be due to an affiliation with a financially weak parent.

Certain non-financial corporates may be partially or fully owned by the government that is willing and able to provide support. In these cases, we incorporate potential support from the government into the final rating of the company by considering the credit strength of the government, the extent to which the government and the supported company are closely integrated and/or jointly susceptible to adverse circumstances that could weaken their financial position and the likelihood that the government’s support, when needed, would be provided in a timely manner.

For government-owned entities with some form of special legal status and/or public policy mandate, and a high level of operational and financial linkage with the government, we may view these entities to be closely integrated with the government and apply a top-down approach to assign credit ratings that are either on par with the government or notched down from the rating level of the government, depending on our view on the likelihood of timely support from the government, when needed.

After considering the rating factors and other rating considerations, we typically assign an issuer or senior unsecured rating to companies rated under this methodology.

Individual debt instrument ratings may be notched up or down from the issuer rating or the senior unsecured rating to reflect our assessment of relative differences in expected loss related to an instrument’s seniority level and collateral.

Our analysis for holding companies considers structural subordination as well as the diversification or concentration of cash flows available to the holding from its subsidiaries and issuer-specific support arrangements.

This credit rating methodology does not include an exhaustive description of all factors that we may consider in assigning credit ratings in the sectors covered in this methodology. Non-financial corporates may face new risks or new combinations of risks, and they may develop new strategies to mitigate risk. We seek to incorporate all material credit considerations in credit ratings and to take the most forward-looking perspective where we have sufficient information and visibility.

Ratings reflect our expectations for a company’s future performance; however, as the forward horizon lengthens, uncertainty increases, and the utility of precise estimates typically diminishes. In most cases, nearer-term risks are more meaningful to issuer credit profiles and thus have a more direct impact on ratings. However, in some cases, our views of longer-term trends may have an impact on credit ratings.

The information used in assessing the factors and sub-factors is generally based on information provided by the company, including financial statement disclosures and publicly available data, such as disclosures by regulators. We may also incorporate non-public information.

While our credit ratings reflect both the likelihood of a default on contractually promised payments and the expected financial loss suffered in the event of default, our approach in this credit rating methodology to assess individual standard rating factors and considerations and instrument-level notching is principally intended to capture fundamental characteristics that drive going-concern credit risk. As a debt instrument becomes impaired or defaults or is very likely to become impaired or to default, our credit ratings typically include additional considerations that reflect our expectations for recovery of principal and interest, as well as the uncertainty around that expectation.

Our forward-looking opinions are based on assumptions that may prove, in hindsight, to have been incorrect. Reasons for this could include unanticipated changes in any of the following: the macroeconomic environment, general financial market conditions, sector competition, disruptive technology, or regulatory and legal actions. In any case, predicting the future is subject to substantial uncertainty.

[1] Credit rating methodologies describe the analytical framework that credit rating councils of VIS Rating use to assign credit ratings. Methodologies set out the key analytical factors that VIS Rating believes are the most important determinants of credit risk for the relevant sector. However, credit rating methodologies are not exhaustive treatments of all factors reflected in VIS Rating’s credit ratings.

[2] Refer to VIS Rating ‘s Rating Symbols and Definitions

Tiếng Việt

Tiếng Việt

English

English