VIS Rating - An Affiliate of Moody's presents our update on the 2024 full-year financial performance of securities firms.

Here's what you need to know:

☑️ Overall, credit fundamentals for securities firms improved in 2024 from the prior year. The sector return on average assets (ROAA) rose by 20bps to 4.5% in 2024, driven mainly by stronger margin lending and fixed-income investment gains of the large firms. In addition, asset risks stabilized as firms cut back on offering commitments for bond buyback and bond defaults slowed. Sizeable capital raised from large and private bank-affiliated firms kept the sector leverage at a low level. In 2025, we expect the sector credit fundamentals will continue to improve from stronger margin lending and bond distribution.

Exhibit 1: Credit fundamentals for securities firms improved in 2024 from the prior year

| 7 | 15 | 8 |

Source: VIS Rating

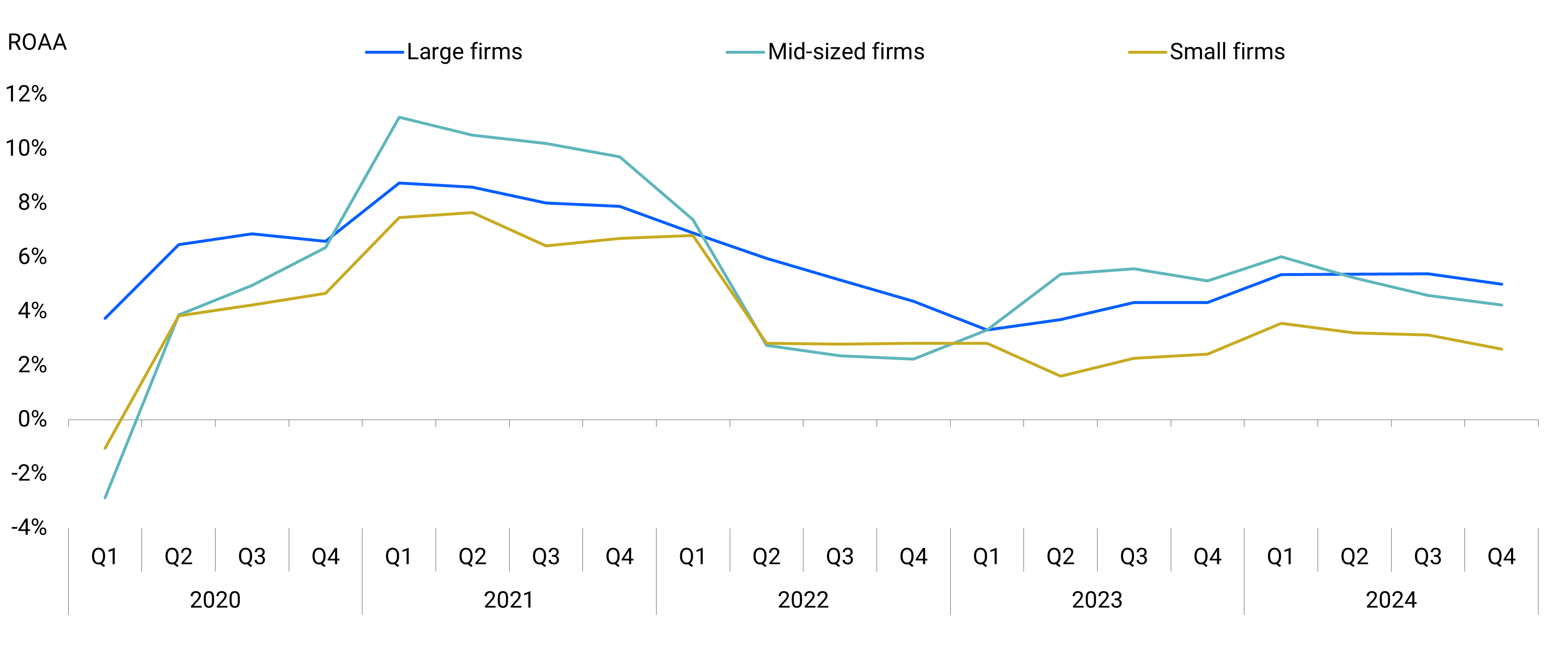

Exhibit 2: Large firms’ profitability outperformed peers’ from stronger margin lending income and fixed-income investment gains

Note: Data includes top 30 securities firms by assets, covering around 90% of total sector assets

Source: Company data, VIS Rating

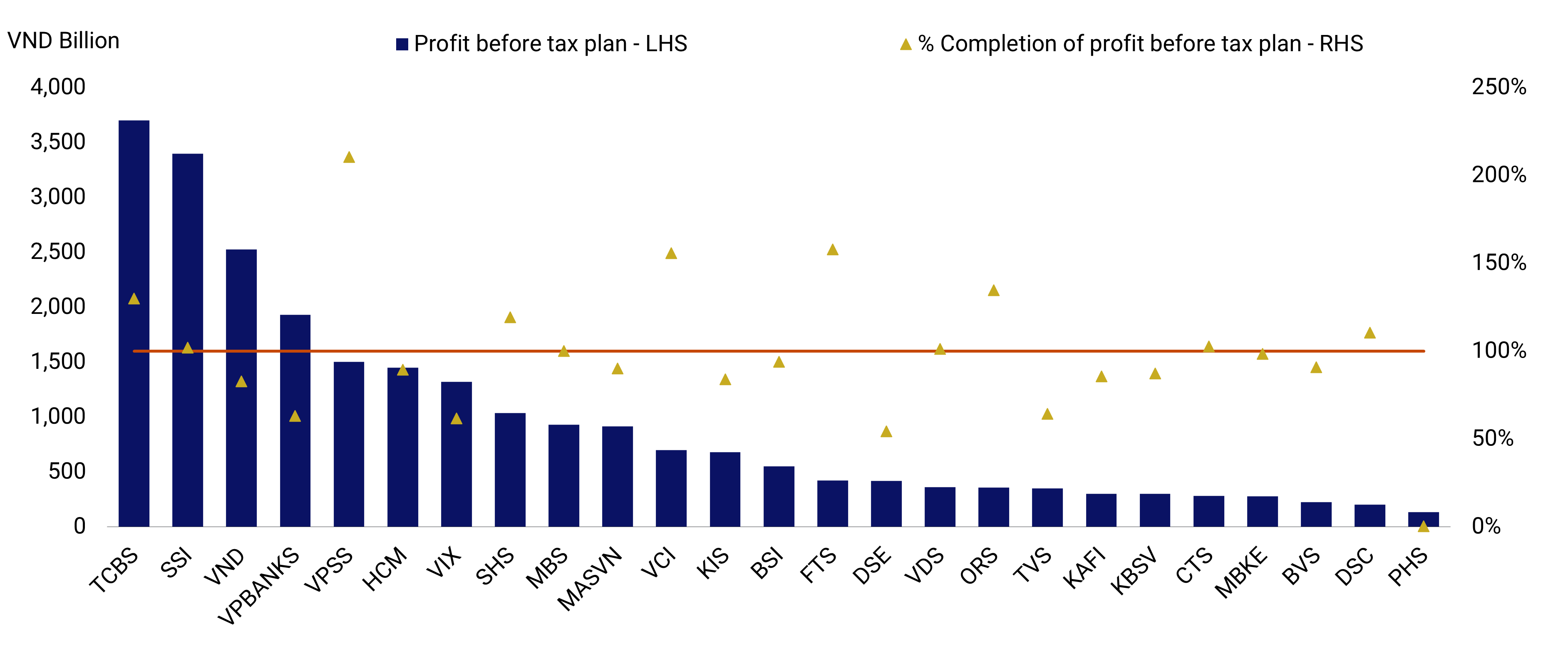

Exhibit 3: Mainly large and private bank-affiliated firms achieved their full-year 2024 profit targets

Source: Company data, VIS Rating

“Large firms led sector profit growth in 2024, driven by stronger margin lending and fixed-income investment gains. Their ROAA rose from 4.3% in 2023 to 5.0% at the end of 2024. Among these firms, VCI and SSI recorded stronger-than-peer margin loan growth backed by their extensive brokerage customer base. Meanwhile, other large firms including private bank-affiliated firms recorded higher fixed-income investment gains (e.g., VPSS), and bond advisory fees (e.g., ORS, TCBS). VND saw a significant profit decline in 4Q2024, driven by higher credit costs related to its credit exposure to a large power sector corporate group. Smaller firms recorded significant decline in equity investment income and ROAA (e.g., VIX, VDS) as stock market valuation declined in 2H2024.

Looking ahead, we expect private bank-affiliated firms will continue to lead sector profit growth in 2025 by leveraging their customer networks and capital from parent banks to expand margin lending and bond distribution activities.

In addition, we expect exposure to event risk to remain high for these firms as they increased margin lending to large customers in 2H2024 amid sluggish demand from retail customers,” – Nguyen Ha My, CFA – Associate Analyst, VIS Rating.

Be among the first to receive our research updates and receive invitations to our events, sign up to be on our mailing list: https://visrating.com/

Follow VIS Rating - An Affiliate of Moody's on our LinkedIn and Facebook pages, and engage with us as we work together to navigate the credit themes and issues critical for issuers and investors.

Contact our Head of Ratings and Research, Simon Chen (simon.chen@visrating.com, simon.chen@moodys.com) if you would like to meet with our analysts and discuss further.

#visrating #vietnam #sectorupdate #creditratings #teammoodys #securitiessector

Tiếng Việt

Tiếng Việt

English

English