VIS Rating - An Affiliate of Moody's presents our credit view on the first transitional renewable project to finalize selling price with EVN.

In April 2025, Gia Lai Electricity JSC (GEG) announced that it had reached an agreement with Vietnam Electricity (EVN) on the official selling price of the Tan Phu Dong 1 wind power plant (TPD1). TPD1, commenced operations in June 2023, is the first transitional renewable energy project reaching a selling price agreement with EVN. TPD1 is among the 85 solar and wind power transitional projects that completed construction in 2021-2022 but failed to meet the requirements and deadlines to be eligible for the government’s FIT rates.

“We expect the agreement on the selling price and retroactive payment for TPD1 will strengthen GEG’s profitability and debt serviceability. In addition, the agreement will pave the way for the remaining 84 transitional renewable energy projects to accelerate negotiations with EVN and finalize the selling price and other terms and conditions. We view transitional projects’ selling price agreements with EVN will improve their debt coverage from weak levels and reduce the high bond default rate in the renewable energy sector,”– Le Viet Cuong – Associate Analyst, VIS Rating

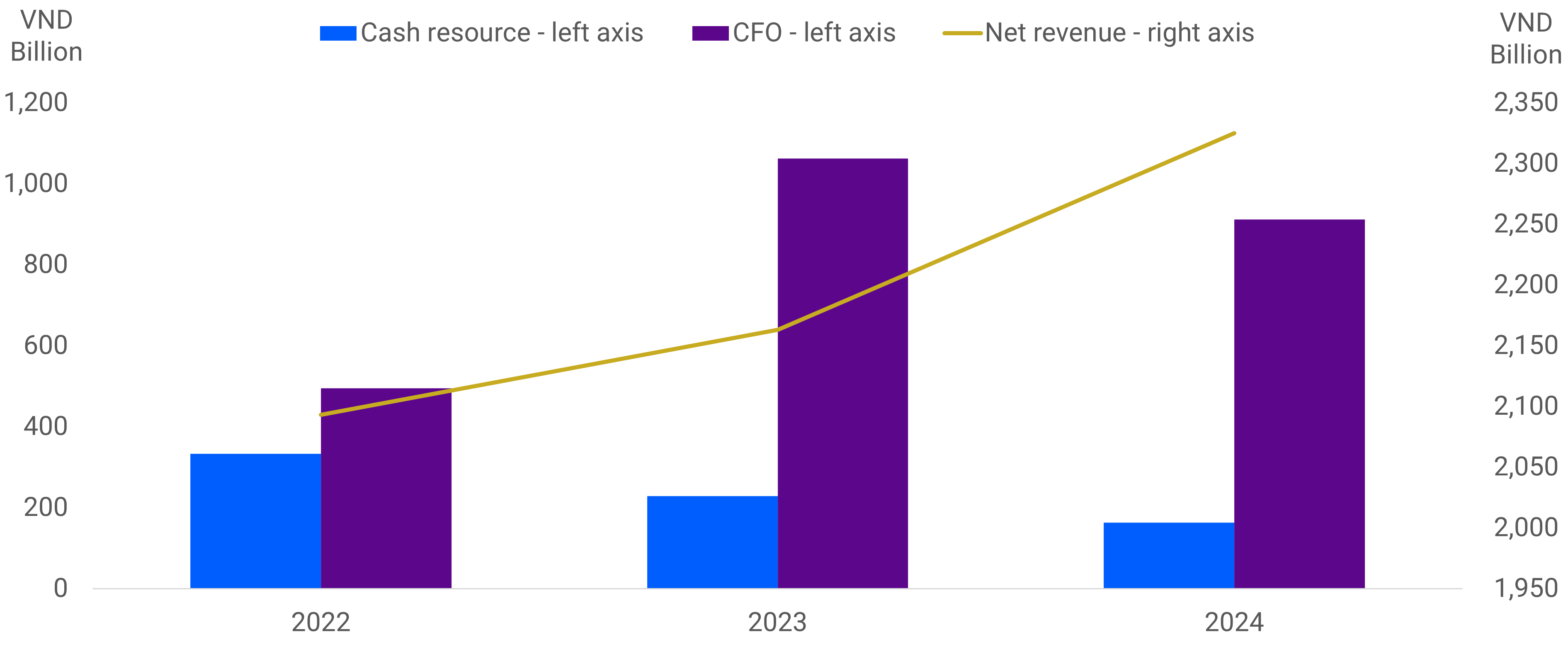

🔹 GEG agreed with EVN on a selling price of VND 1,813/kWh for TPD1—nearly double the temporary price and close to the ceiling price for transitional offshore wind power (VND 1.816/kWh). The agreement also includes a retroactive payment of around VND 397 billion from EVN for TPD1 ‘s electricity output supplied over the past two years. The finalization of the selling price for TPD1 will enhance GEG’s cash flow and debt serviceability. In particular, EVN’s retroactive payment will improve GEG’s Debt/EBITDA to 3.9x - 4.2x (2024: 5.2x) and CFO/Debt to 14% - 16% (2024: 10%).

🔹 Key terms of the agreement cover not only price but also output volume, acceptable loss parameters, total investment cost, and optimal financial metrics. Based on this precedent, other transitional projects can accelerate their price negotiation with EVN. We anticipate that future price agreements for transitional projects will feature official prices that are significantly higher than the temporary rates, along with corresponding retroactive payments, as seen in the TPD1 case. Thereby, these agreements will help to improve debt serviceability and halt new bond defaults in companies related to transitional projects. As of March 2025, 90% of VND 19 trillion of power defaulted bonds linked to transitional projects, causing the default rate of 40%.

TPD1 price agreement will improve GEG’s financial performance in 2025

Source: Company data, VIS Rating

Be among the first to receive our credit outlook reports, hear about our research updates and receive invitations to our events, sign up to be on our mailing list: https://visrating.com/

Follow VIS Rating - An Affiliate of Moody's on our LinkedIn and Facebook pages, and engage with us as we work together to navigate the credit themes and issues critical for issuers and investors.

Contact our Head of Ratings and Research, Simon Chen (simon.chen@visrating.com, simon.chen@moodys.com) if you would like to meet with our analysts and discuss further.

#visrating #vietnam #power #GEG #creditratings #teammoodys

Tiếng Việt

Tiếng Việt

English

English