VIS Rating - An affiliate of Moody's presents our update on the 2024 full-year financial performance of Top 24 listed industrial real estate developers by revenue.

Here's what you need to know:

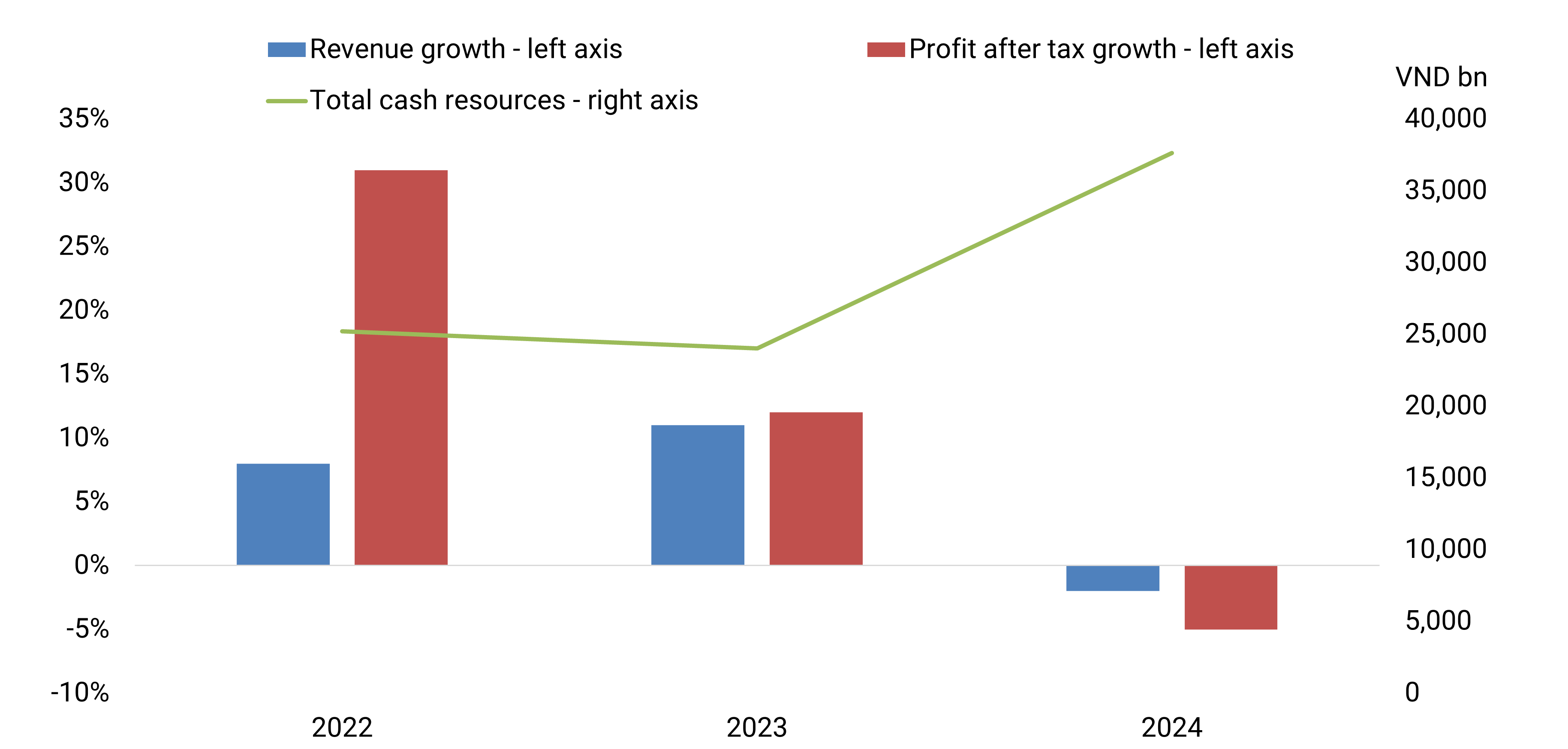

☑️ In 2024, our covered developers’ revenue and profit slightly decreased by 2%, and 5% year-over-year (YOY), respectively, following three consecutive years of growth. This decline in revenue was driven by a decline in new FDI tenants (VRG, -79% YOY and VGC - a subsidiary of GEX (A, stable) -10% YOY) as well as lower land handover caused by prolonged legal obstacles (KBC, -51% YOY). Meanwhile, some developers in the South with substantial leasable facilities (e.g., IDC, SIP, SNZ) recorded 15-30% YOY growth in revenue.

☑️ Leverage, represented by the sector average Debt/EBITDA, increased from 2.0x at end-2023 to 2.8x at end-2024, reversing the declines during 2019 and 2023. Developers increased debt financing for land bank expansion following the roll-out of new laws that accelerated legal procedures and project development. Developers’ total debt increased significantly in Q4/2024 by 30% YOY, mainly driven by NTC (+867%), KBC (+176%), ITA (+175%), and SIP (113%). Approximately 75% of the new debt in 2024 was long-term debt, which raised the long-term debt composition from 58% at the end of 2023 to 62% at the end of 2024. Using more long-term debt to finance land expansion will help developers reduce the risk of maturity mismatch between the debt and the cash flow received.

☑️ The sector’s liquidity remained strong, supported by robust cash resources and stable operating cash flow (CFO). CFO increased slightly by 6% YOY in 2024 from strong customer advances, which accounted for around 32% of total assets over the last 3 years. A rise in new advance payment for IDC (96.4ha at Huu Thanh, Phu My 2 and Que Vo 2 industrial parks) and SIP (74ha at Phuoc Dong, Loc An – Binh Son and Le Minh Xuan 3 industrial parks) boosted these companies’ CFO, even though the revenue will be recognized later upon completing the handover of land and related legal procedures to the customer.

“We expect increasing sales for industrial park developers in 2025, driven by stronger supply and demand for new industrial land. Accelerated legal procedures and the completion of the provincial masterplan will enable developers to expand their land banks and enhance new supplies. Increased investment in public infrastructure and supportive policies to attract FDI will boost industrial park leasing demand, subsequently increasing new sales for developers,”– Hoang Thi Hien – Associate Analyst, VIS Rating.

Exhibit 1: Despite a slight decline in revenue and profit recognition, the sector’s liquidity remained strong, supported by robust cash resources

Note: Top 24 listed industrial real estate developers in terms of revenue

Source: Company data, VIS Rating

Be among the first to receive our monthly corporate bond reviews, hear about our research updates, and receive invitations to our events, sign up to be on our mailing list: https://visrating.com/

Follow VIS Rating - an affiliate of Moody's on our LinkedIn and Facebook pages, and engage with us as we work together to navigate the credit themes and issues critical for issuers and investors.

Contact our Head of Ratings and Research, Simon Chen (simon.chen@visrating.com, simon.chen@moodys.com) if you would like to meet with our analysts and discuss further.

#visrating #vietnam #industrialrealestate #creditratings #teammoodys

Tiếng Việt

Tiếng Việt

English

English